Source: CoBank Quarterly

Animal protein demand remains exceptional

The brightest spot in the animal protein segment over the past couple of years has been consumer demand. Americans are still overwhelmingly choosing protein as retail meat department dollar sales were up 6.8% and unit sales were 2% higher for the 52 weeks ending January 2026, according to Circana sales data.

Labor cost at the foodservice level is one of the largest contributors for the jump in the food away from home metric. As labor and other necessary input costs became more expensive, menu prices had to reflect the changes. More quick-service restaurants (QSRs) are featuring chicken items over hamburgers or beef to help keep margins afloat alongside all other rising costs.

Poultry

A stockpile of U.S. corn continues to benefit animal feeders, specifically the U.S. broiler segment, the animal protein sector with the quickest production cycle. However, even with feed costs sitting about 20% below year ago levels to end 2025, broiler production costs at the end of 2025 were still 10% to 15% higher than pre-COVID-19 inflation-era levels.

These higher costs have kept the industry laser-focused on efficiencies. The broiler hatchery supply flock was down 2% YoY in February, yet eggs hatched were up 2% YoY from the productive flock during January. This highlights just one of the areas where data tells us the industry is continually working towards doing more with less.

With these improved efficiencies, broiler slaughter totals are running about 4% higher than the same period a year earlier through the first 10 weeks of 2026. Despite these improvements, flock health, hatchability and mortality continue to be concerns, and we expect these challenges to dampen broiler output growth prospects in 2026.

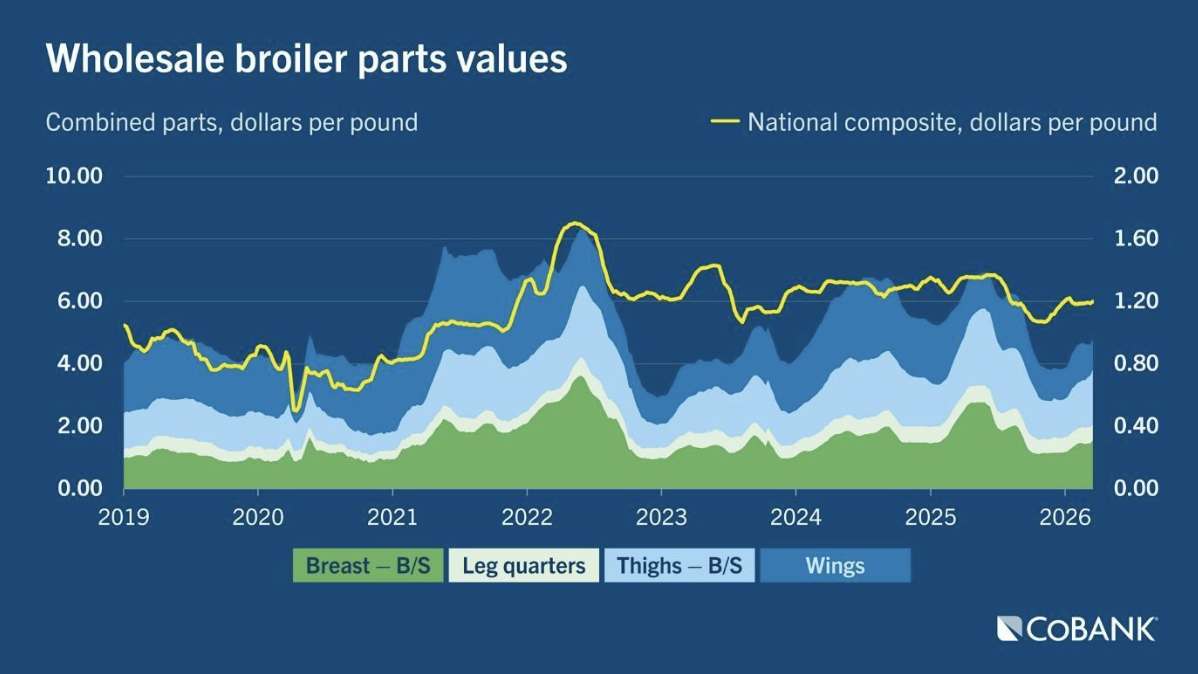

Processor margins were exceptionally strong for the first half of 2025 as a result of favorable feed costs and historically strong broiler meat prices. But during the fourth quarter, oversupply issues resulted in softening broiler values. Winter storms and rising liveweights have contributed to excess market availability and the market has yet to regain composure. Breast meat values have remained unseasonably flat at about $1.50 per lb. – 15% below last year’s annual average as of late. While margins have been pressured in recent months, the lower values are expected to spur marketing for chicken features in both the restaurant and grocery segments for spring and summer.

.png)